Managing the finances of a parent or spouse who needs ongoing care is one of the more demanding tasks a family can face.

The costs are real and often unpredictable – assisted living, in-home care, memory care, medical equipment, prescription drugs – and the tax rules and Medicaid eligibility requirements that apply to them are genuinely complicated.

Getting this wrong costs money. Getting it right can make a meaningful difference in what care is affordable.

Where the Numbers Get Complicated

Senior care expenses sit at the intersection of several financial systems that don’t always talk to each other clearly: Medicare, Medicaid, Social Security, retirement accounts, and the federal tax code.

Most families navigate this without professional guidance, which means they miss deductions they’re entitled to, mismanage asset transfers that affect Medicaid eligibility, or take retirement income in ways that create unnecessary tax exposure.

Working with accounting and bookkeeping assistance experienced in elder care finances makes a real difference here.

The rules are specific enough that general financial advice often misses the details that matter most in this situation. The expenses that most commonly create confusion include:

- Long-term care facility costs – which portion qualifies as a medical deduction depends on the level of care received

- In-home aide expenses – deductible when the primary reason is medical, not just companionship or daily tasks

- Home modifications for medical reasons – ramps, grab bars, widened doorways

- Prescription drugs and medical equipment not covered by Medicare

- Home modifications for medical reasons – ramps, grab bars, widened doorways

- Premiums for long-term care insurance policies

The Medical Expense Deduction

Federal tax law allows a deduction for qualified medical expenses that exceed 7.5% of adjusted gross income. For families paying significant out-of-pocket care costs, this threshold is often reachable – but only if the expenses are properly documented and categorized.

Assisted living costs present a specific challenge. If a resident requires assistance with at least two activities of daily living – bathing, dressing, eating, mobility – or has cognitive impairment, a portion of the facility’s monthly fee may qualify as a medical deduction.

The facility should provide documentation showing what percentage of its services are medical in nature. If they don’t offer this automatically, ask for it.

In-home care is similar. An aide hired primarily to provide medical care or skilled nursing assistance qualifies differently than one hired for companionship or meal preparation. The distinction matters for both tax purposes and for Medicaid look-back calculations.

Medicaid and Asset Management

Medicaid has strict asset and income limits, and most states apply a five-year look-back period to asset transfers. Gifts, transfers to family members, or assets moved into a trust during that window can delay eligibility or reduce benefits.

This is an area where families frequently make costly mistakes without realizing it until the application process begins.

Some assets are exempt from Medicaid calculations – a primary residence in many states, one vehicle, personal belongings – but the rules vary by state and by whether the applicant is single or has a spouse still living at home. A spouse remaining in the community home has different protections than a single applicant.

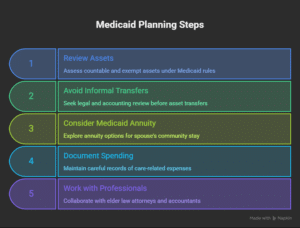

Planning steps worth considering before a care need becomes urgent:

- Review all assets and understand which are countable versus exempt under your state’s Medicaid rules

- Avoid informal asset transfers without legal and accounting review

- Consider a Medicaid-compliant annuity if a spouse needs to stay in the community

- Document all care-related spending carefully – it affects both tax returns and Medicaid applications

- Work with an elder law attorney alongside an accountant, since the legal and financial pieces overlap

Retirement Income and Tax Planning

Social Security benefits, required minimum distributions from IRAs, pension income, and investment withdrawals all interact with each other in ways that affect how much tax a senior pays – and how much of that income Medicaid counts when determining eligibility.

RMDs from traditional IRAs and 401(k)s are taxable income in the year they’re taken. For a senior in assisted living, those distributions may push combined income high enough to make up to 85% of Social Security benefits taxable.

Timing those distributions, or considering a Roth conversion in earlier years, can reduce this exposure significantly.

Long-term care insurance benefits are generally tax-free when used to pay for qualified care. If a policy has a cash indemnity structure rather than a reimbursement model, the tax treatment may differ, but most benefits paid directly for care don’t add to taxable income.

Keeping Records That Hold Up

Whether the goal is a tax deduction, a Medicaid application, or simply understanding where money is going, documentation is what makes everything else work.

Practical records to maintain throughout a care situation:

- Monthly bills and receipts from care facilities, including breakdowns of service categories

- Explanation of benefits statements from Medicare and any supplemental insurance

- Receipts for all out-of-pocket medical expenses, including pharmacy

- Bank statements showing care-related payments

- Any written assessments from physicians or facilities documenting the medical necessity of care

- A spreadsheet tracking monthly expenses by category takes very little time to maintain and pays off significantly at tax time and if a Medicaid application becomes necessary.

Senior care finances don’t get simpler as a care situation progresses. The earlier a family gets organized – and the earlier they bring in professional guidance for the tax and Medicaid pieces – the more options stay available.